Why Stablecoins Matter

Nov 4, 2025

Sending money should be as easy as sending a text message. But today’s payment rails still take hours to days for settlement while charging exorbitant fees.

Stablecoins introduce a 10x improvement, whereby moving money is permissionless, instant, and borderless.

This article explains why stablecoins matter for everyone, from merchants to remittance senders and businesses that transact internationally.

A new paradigm for payments

In a nutshell, stablecoins improve on the existing payment system in four key ways: they’re fast, low-cost, borderless, and available 24/7.

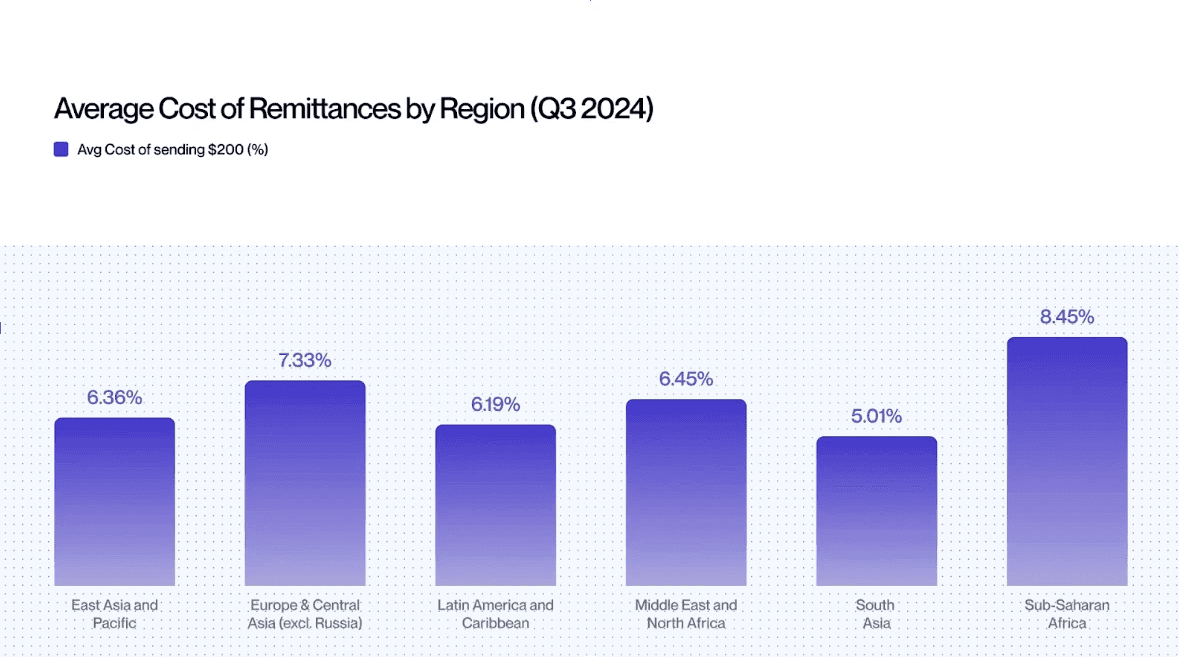

The traditional cross‑border payment system wasn’t designed so much as bolted together. An international transaction often passes through five or more intermediaries, each adding delays and fees.

Stablecoins collapse these layers into a single on‑chain transfer. Emerging markets, home to 85% of the world’s population, stand to benefit the most because they suffer from extractive and archaic financial infrastructure.

Stablecoins currently represent over 1 % of the U.S. money supply, up from just 0.04% in 2020, shedding light on how quickly a new and better monetary layer is forming.

Stablecoins are faster, cheaper, and more accessible

Stablecoins deliver the following benefits that legacy payments can’t match:

1. Speed and Availability: Relative to international bank transfers that can take 2-5 business days to settle, transfers over stablecoin rails typically confirm in under a minute, often just a few seconds. And transfers can be made 24/7, even on weekends and holidays.

2. Cost: Stablecoins are now the cheapest way to send dollars. For example, a remittance payment of $200 via stablecoins costs under $0.01 (0.005%), whereas traditional rails like SWIFT and other remittance corridors can charge between 5-8% ($10 - $16).

3. Programmability and Openness: Unlike the current payments system, stablecoins run on open, programmable blockchains. This means anyone can build applications and financial tools around them.

While some stablecoins like USDC and USDT are permissioned (issuer can freeze or block transfers), they still offer greater flexibility and access than traditional payment rails, especially for developers and users.

4. Financial inclusion: Stablecoins provide a safe, open, and inflation-resistant way for people around the world to spend and save money. They allow the underbanked to bypass the maze of intermediaries within the traditional banking system while sending money across borders.

Stablecoin use cases

People, businesses, and governments are finding new ways to use stablecoins. Here are five concrete real-world use cases:

1. Remittances and Money Transfers

Instead of paying 5-8% in fees and waiting days, with stablecoins, people can move money in minutes at costs as low as one cent.

For example, PayPal already uses its PYUSD stablecoin for international transfers through Xoom. For families in emerging markets, this means that money gets sent faster without being eaten up by middlemen.

2. Corporate Payments

In countries with unstable banking systems, SpaceX collects Starlink revenues by converting local money straight into stablecoins that flow instantly into its treasury.

Other companies like Scale AI pay their contractors in stablecoins to avoid foreign exchange fees and settlement delays, while bank-issued stablecoins like JPMorgan’s JPM Coin moves more than a billion dollars a day between clients.

3. E-Commerce

Companies such as Stripe and Shopify let merchants in 34 countries accept USDC at checkout, with funds settling into local currency or dollars.

Visa offers stablecoin settlement to speed up merchant payouts. And in some Southeast Asian countries, cafés and other shops already let customers pay bills or shop with USDC.

4. Inflation Hedge and Savings

In nations with high inflation, stablecoins act as a digital safety net. For example, in Argentina, Turkey, and Nigeria, millions convert salaries into USDT or USDC right away to protect their savings. More than 60% of crypto activity in Argentina and about half in Turkey is already in stablecoins.

Additionally, yield-bearing stablecoins like Noble Dollar (USDN) offer a way for individuals to benefit from the safety of holding a dollar-backed stablecoin while accruing ~4% on their principal via short-term U.S. Treasury bonds.

5. Governments

Even governments have started to recognize the benefits of stablecoins. Recently, Wyoming became the first U.S. state to issue its own dollar-backed stablecoin. Wyoming launched the Frontier Stable Token (FRNT) as a fully reserved USD stablecoin on multiple blockchain networks like Ethereum, Solana, and Avalanche.

Conclusion

Stablecoins matter because they make money programmable, open, cheaper, and faster for all.

They slash remittance fees, give businesses more control over cash, and enable new financial products that weren’t possible in the era of siloed banking networks.

Instead of waiting days or paying unnecessary fees, users can now send, save, and build with digital money that works anytime, anywhere, and for anyone.