Stablecoins and Monetary Policy

Dec 4, 2025

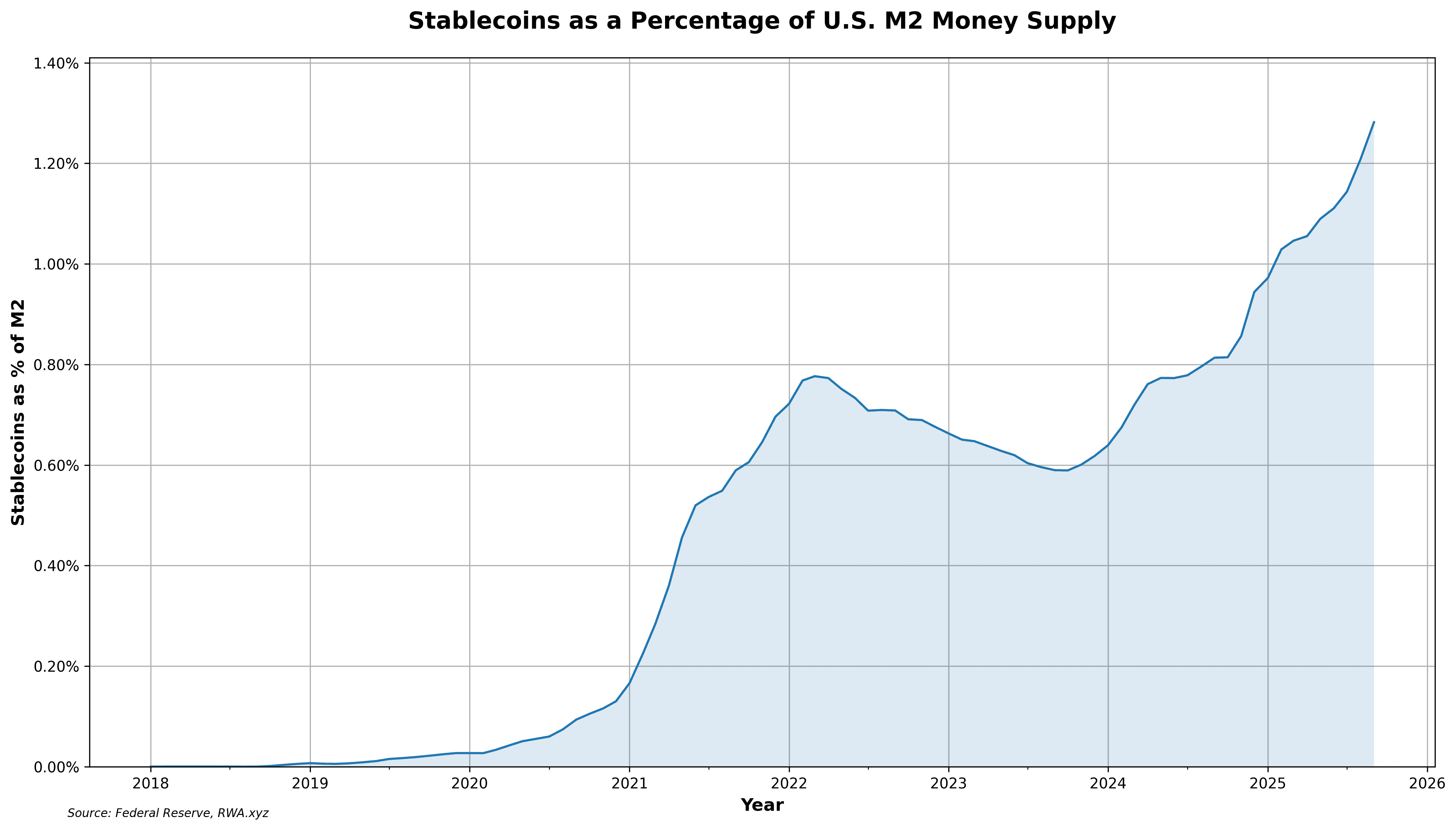

Stablecoins today represent 1.3% of U.S. M2 supply (a measure of money supply) - a 5,000x increase since Jan 2018. Recent estimates by the Federal Reserve suggest that the overall stablecoin supply, currently at $304B, could hit $1 - $3 trillion (a 10x increase) by the end of the decade. For reference, during the COVID-19 pandemic, the Fed increased its holdings of U.S. Treasuries by roughly $3 trillion through quantitative easing. Approximately $7 trillion of U.S. Treasuries are outstanding today.

If the Fed's estimates of stablecoin expansion prove to be accurate, their impact on monetary policy cannot be ignored. According to Azzimonti and Quadrini, widespread adoption of stablecoins at this scale could put as much as 40 basis points of downward pressure on interest rates.

The GENIUS Act has brought further legitimacy to stablecoins. By defining a clear framework for issuance and reserves, it lowers regulatory uncertainty, makes it easier for institutions to participate, and is likely to accelerate stablecoin adoption and fuel growth.

In this blog post, we discuss five monetary policy implications for both the U.S. and the rest of the world that arise from increased global dollarization driven by higher demand for dollar-denominated stablecoins.

Implications for U.S. and Global Monetary Policy

1. A global stablecoin glut

Earlier this month, Fed economist Michael Miran drew a comparison between projected stablecoin growth and the ‘global saving glut’ during the early 2000s.

From 1996 to 2004, countries running large trade surpluses accumulated massive dollar reserves from selling goods to the U.S. They recycled those dollars back into American assets, particularly Treasuries.

According to the Fed Chairman back then, Ben Bernanke, this caused the U.S. current account deficit (value of imports greater than exports) to widen by 4 percentage points of GDP. This foreign demand for Treasuries pushed down interest rates across the economy.

Stablecoins create a similar effect. A stable, dollar-denominated instrument is particularly attractive for individuals and institutions in countries with volatile currencies or capital controls. When these foreign entities buy stablecoins, issuers (like Circle or Tether) must purchase Treasuries to back them. The extra demand pushes bond prices up and yields down. The result is a downward pressure on interest rates, similar to the global saving glut.

According to Miran, $2 trillion in foreign stablecoin demand would increase the current account deficit by 1.2 percentage points of GDP. That's 30% of the original global saving glut. A more bullish $4 trillion scenario causes the deficit to widen by 60% of the global saving glut.

2. Lower monetary wiggle room

An increased foreign demand for USD stablecoins puts downward pressure on the neutral rate of interest (r*). The neutral rate of interest is the real interest rate (accounted for inflation) that would prevail when the economy is at full employment with stable inflation. It is a theoretical construct but has real implications for the economy. For example, when r* falls but the Fed doesn't cut policy rates accordingly, policy becomes contractionary, and the economy slows down (and vice versa).

A lower r* leads to a binding zero lower bound (ZLB), meaning that during a period of recession, the Fed will have less room to cut interest rates before hitting zero.

For example, if r* is at 2.5% with 2% inflation, the nominal rate is 4.5%. The Fed has 4.5 percentage points of ammunition in a recession.

But if stablecoins push r* to 1.5%, the nominal rate becomes 3.5%. The Fed now only has 3.5 percentage points to work with before it hits zero. This could, for instance, cause recessions to be deeper and longer.

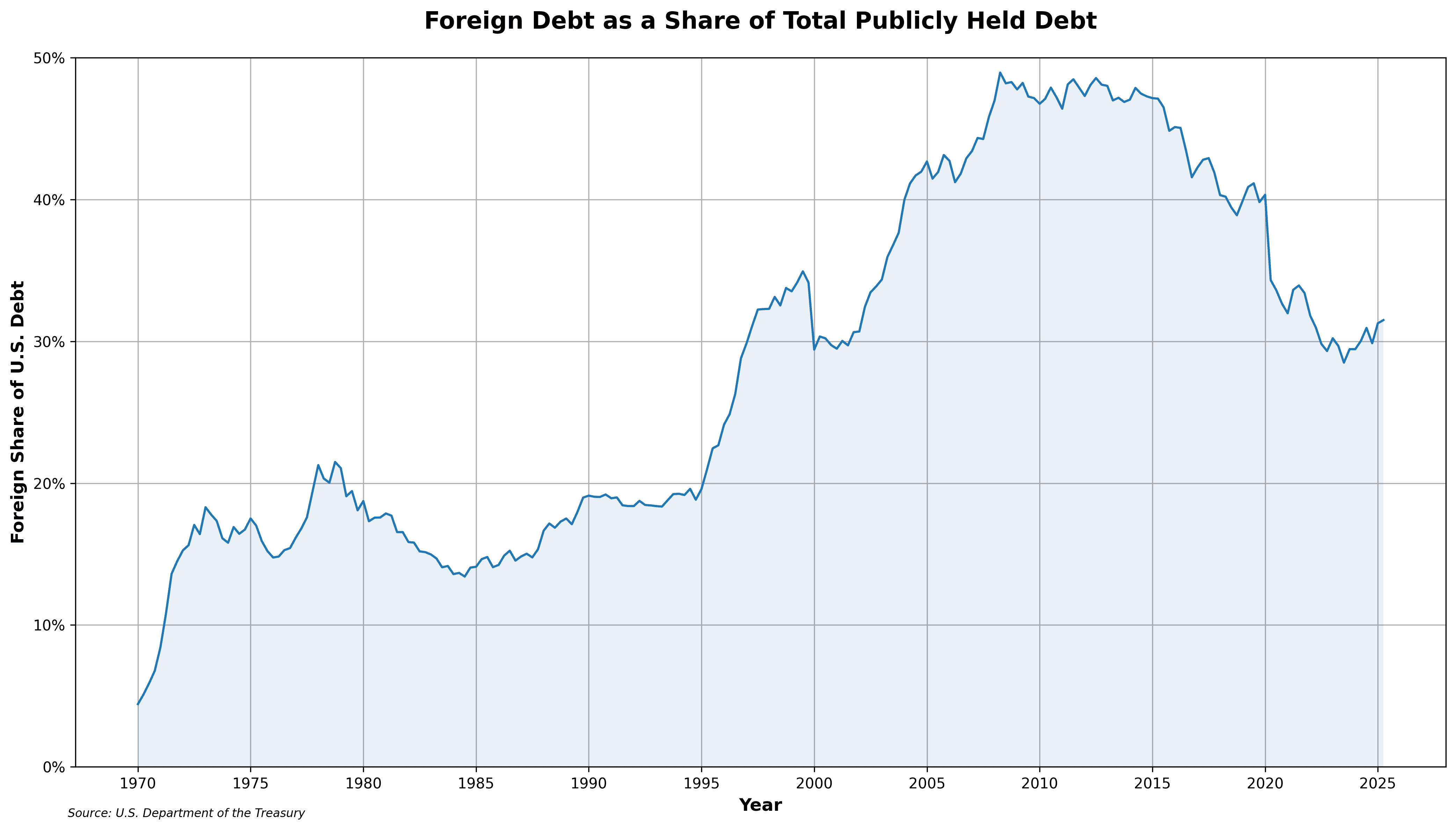

3. A new channel for America’s 'Exorbitant Privilege'

The U.S. has benefited from what French Finance Minister Valéry Giscard d'Estaing called the ‘exorbitant privilege’ in the 1960s, referring to the country’s ability to borrow cheaply in its own currency while the rest of the world holds dollars as reserves. This lets the U.S. run persistent current account deficits without triggering a currency crisis. The country can, in effect, spend more than it makes because foreign entities want dollar assets.

But this privilege is now under pressure. Foreign holdings of U.S. debt peaked near 50% during the Great Recession, then declined to around 30% this year. China and other countries have been diversifying away from Treasuries. The share of global foreign exchange reserves held in dollars has dropped from over 70% in 2000 to around 58% today.

In this context, rising global demand for dollar-denominated stablecoins may represent a new, bottom-up form of the U.S.’s privilege - one driven less by foreign central banks and more by households and businesses seeking direct access to the dollar system.

4. Floating exchange rates become less impactful

Floating exchange rates act as economic shock absorbers. When a country's economy weakens, its currency depreciates, and therefore, exports become cheaper, tourism picks up, etc.

For example, suppose Mexico’s economy weakens, and the peso moves from 20 to 25 per dollar. A Mexican manufacturer selling furniture for 10,000 pesos gets the same 10,000 pesos whether the exchange rate is 20 or 25. But for a U.S. consumer, the price falls from $500 at 20 pesos per dollar to $400 at 25 pesos per dollar.

Global dollarization via widespread dollar-denominated stablecoins makes floating exchange rates less effective because if businesses and households use dollar stablecoins for transactions (goods and services are now denominated in USD), the local currency can't depreciate to cushion shocks. Instead, the adjustment will happen via real changes in the economy, like unemployment and lower output.

5. Money creation moves outside of banking channels

When you use the money in your bank account to buy stablecoins, the following happens:

Your bank deposit shrinks, and your stablecoin balance goes up.

The stablecoin issuer takes the dollars it received from you and buys U.S. Treasuries.

Over time, that extra demand helps the U.S. government roll over and issue debt more cheaply, and the resulting government spending increases the money supply in the economy.

In this scenario, traditional bank lending plays no role. The central bank's usual transmission mechanism doesn't work, i.e., when banks make loans, they lose reserves held at the central bank and must refinance by borrowing from the central bank or other banks at rates set by the Fed (called the interbank rate). That's how Fed policy affects lending rates throughout the economy. But money created through stablecoin purchases bypasses this model.

Businesses still need bank loans for operations and expansion. Stablecoin issuers don't lend to companies or households. But as stablecoins scale, the composition of money creation shifts. If $2-3 trillion enters through government spending (financed by stablecoin Treasury purchases) rather than private sector bank credit, the Fed has less control over credit conditions where businesses actually operate and invest.

Conclusion

Stablecoins don’t overturn U.S. monetary policy, but they do impact the background conditions in ways that will be hard to ignore. The real opportunity is not in replacing banks, but as Miran put it, “to satiate the untapped foreign appetite for dollar assets from savers in jurisdictions where dollar access is limited”.

If issuance expands into the low multi-trillion range, that incremental demand for stablecoins will quietly reshape how global savings reach the U.S., how much policy ammunition the Fed has, and the degree to which world economies become increasingly interdependent.